The rapid advancement of artificial intelligence, particularly from Chinese developers, is sparking a debate about its potential to either exacerbate or alleviate economic inequality on a global scale. While the United States has long been considered the leader in AI development, Chinese companies like DeepSeek have emerged as formidable competitors. The release of a new Chinese AI model last year reportedly "terrified U.S. markets and sunk NVIDIA's stock price," according to NPR's The Indicator from Planet Money.

This heightened competition, driven in part by the availability of open-source large language models (LLMs) and more competitive pricing strategies from Chinese firms, could fundamentally alter the AI landscape. The argument presented is that this competitive pressure can lead to lower costs for AI products and services, ultimately benefiting consumers worldwide. This dynamic challenges the prevailing narrative that AI is an inevitable engine of inequality, where automation leads to widespread job displacement and concentrated wealth among a few tech giants.

Dean Baker, a Senior Fellow at the Center for Economic and Policy Research, posits that robust competition in the AI sector could indeed serve as a leveling force. He makes the case that competition could even the playing field. When more than one company is offering a similar product, the costs go down for everybody, and that benefit flows to consumers. This increased availability and affordability of AI tools could democratize access to powerful technologies, fostering innovation and productivity across a wider range of industries and individuals.

However, some analysts express caution regarding the extent to which Chinese AI competition can counteract the trend of increasing inequality. Darian Woods, a co-host of NPR's Planet Money, acknowledges that it's an "intriguing thesis" but points out that Chinese competition hasn't prevented the rise of trillion-dollar big tech companies prior to the current AI boom. This historical context suggests that market dominance and wealth accumulation by a few major players may be a persistent feature of the technology sector, regardless of the origin of the leading AI innovations. The concentration of power and profits in the hands of a few large corporations has been a trend observed in previous technological revolutions.

The implications of this competitive dynamic extend beyond market share and pricing. The development of advanced AI capabilities by a wider array of global players could accelerate the pace of innovation, leading to new applications and solutions across various sectors. This could include advancements in areas that directly address societal challenges, such as healthcare, education, and resource management. The open-source movement, in particular, plays a crucial role in disseminating AI technologies, enabling smaller businesses and researchers to leverage these powerful tools without prohibitive upfront costs.

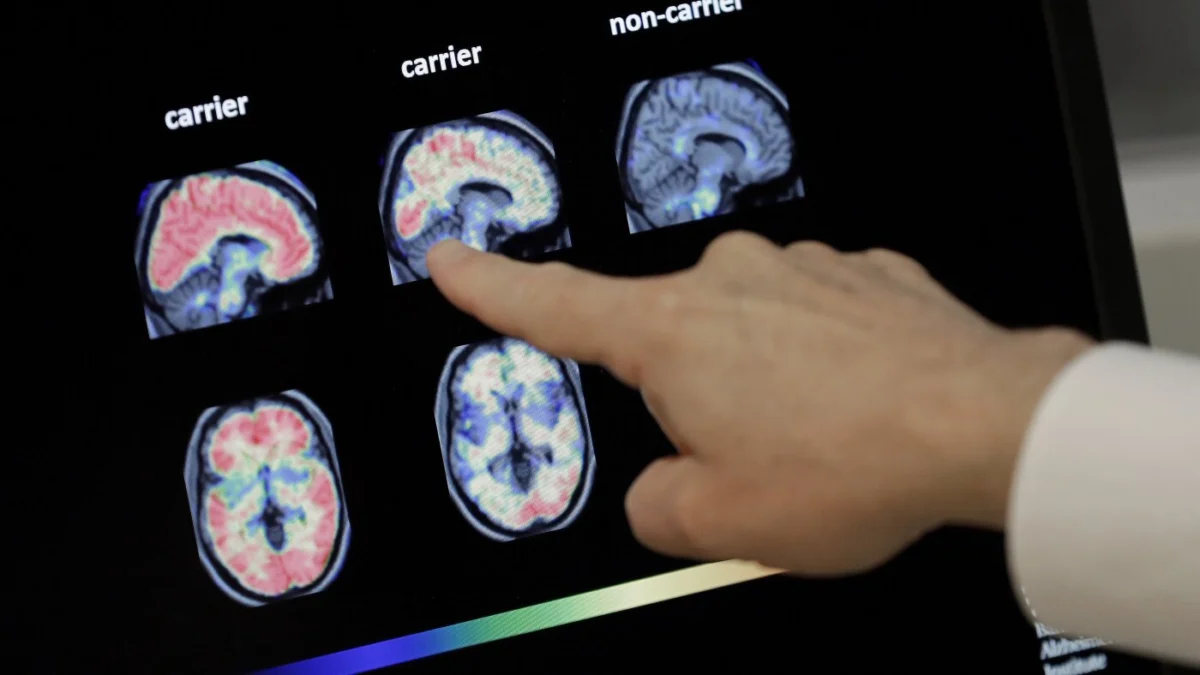

Beyond the realm of artificial intelligence, another pressing economic concern highlighted involves the financial vulnerability of individuals with dementia. Research indicates a significant correlation between the onset of dementia and a loss of personal wealth, often occurring years before a formal diagnosis. This cognitive decline impairs an individual's ability to manage complex financial matters, leading to potentially devastating financial consequences.

Lauren Nicholas, a health economist and professor of geriatrics at the University of Colorado, has conducted new research finding that wealth starts to decline approximately six years before a dementia diagnosis. She explains there's a close connection between dementia and a loss of personal wealth, as dementia is one of the diseases where individuals lose cognitive capabilities over time that are unfortunately closely tied to our ability to manage our own money.

During this period of cognitive decline, individuals may fall victim to financial scams, make poor investment decisions, or neglect essential financial responsibilities such as paying taxes. The cumulative effect of these financial missteps can lead to the depletion of savings and significant debt accumulation.

Sanda Balaban's personal experience with her father illustrates this issue starkly. Upon visiting him after years of estrangement, she discovered his office in disarray, filled with financial documents. These revealed credit card statements showing her dad was spending thousands of dollars a month on "scammy health products and online subscriptions." She also learned he hadn't paid income tax since 2014 and had drained his savings. Her father had, in essence, depleted his life savings due to the cognitive impairments associated with his undiagnosed dementia.

The challenge in addressing this problem lies in early detection and intervention. Financial advisors, who might be expected to notice such financial deterioration, often feel ill-equipped or hesitant to broach the subject with clients. A survey from the investment firm Fidelity shows that advisors "didn't feel comfortable raising the issue for fear of being wrong." This reluctance creates a critical gap in the support system for individuals at risk.

The financial red flags associated with dementia can manifest in various ways, including unusual spending patterns, missed bill payments, and a general disorganization of financial affairs. These are often subtle indicators that can be easily overlooked by family members or even financial professionals until the situation becomes severe. The progressive nature of dementia means that these financial management issues tend to worsen over time, making timely intervention crucial.

Developing effective solutions requires a multi-faceted approach. This could involve greater awareness among financial professionals about the signs of cognitive decline and training on how to sensitively address these concerns with clients and their families. Furthermore, technological solutions, perhaps even AI-driven tools, could be developed to monitor financial activity for anomalies indicative of cognitive impairment, flagging potential issues for review by trusted individuals or professionals. The goal is to create a safety net that protects vulnerable individuals from financial exploitation and mismanagement as their cognitive abilities decline.